Credit: Creative Commons @WikiVisuals

Define “co-insurance”. What about “premium”? If you’re struggling with answers, you’re not alone.

A high percentage of Americans have trouble with such standard health insurance terms, calling the whole process of selecting a plan confusing and stressful, surveys and studies from the past few years have shown.

Ever since the Affordable Care Act (ACA) rolled out and brought 20 million more people into the fold, health insurance literacy has been a glaring issue – one that needs constant attention, experts say, no matter what direction health care heads in.

Choosing coverage can be complicated and is perhaps one of the most dreaded decisions people make, yet it’s also one of the more important ones because of the consequences. Confusion about key terms or misunderstanding of the information can leave people in a precarious position.

“We observe great challenges with health insurance literacy,” said Daniel Polsky, PhD, executive director of Penn’s Leonard Davis Institute of Health Economics (LDI) and professor of Medicine in the Perelman School of Medicine. “What happens is that people get overwhelmed by the choices and end up not purchasing health insurance at all, or they participate in the market and they make suboptimal decisions.”

One example is the ACA’s Cost Sharing Reduction, which gives a break on co-pays, co-insurance, and deductibles for those with a low enough income. “A lot of people who qualified for this benefit did not receive it because of challenges with health insurance literacy,” he said. “That could be a multi-thousand-dollar mistake.”

The data are sobering.

A Health Insurance Cheat Sheet

Deductible: The amount you pay for covered health care services before your insurance plan kicks in. With a $2,000 deductible, for example, you pay the first $2,000 of covered services yourself.

Co-pay: A fixed amount ($20, for example) you pay for a covered health care service, such as a doctor’s visit or drug prescription.

Co-insurance: The percentage of costs of a covered health care service you pay (20%, for example) after you've paid your deductible.

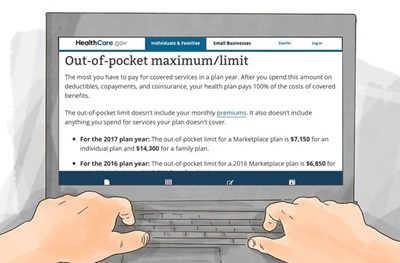

Out-of-pocket maximum: The most you have to pay for covered services in a plan year.

Premium: The amount you pay for your health insurance every month, be it through an employer or insurance you obtained through the ACA.

Source: Healthcare.gov

A recent survey from Policy Genius found that just four percent of Americans correctly defined “deductible,” “co-pay,” “coinsurance” and “out-of-pocket maximum.” Millennials scored the worst, a trend spotted two years earlier in a Penn Medicine study. Younger people were confused by the words “deductible” (48 percent defined incorrectly) and “co-insurance” (78 percent defined incorrectly) when signing up through Healthcare.gov, the Penn researchers reported.

Another survey published last month from the University of Connecticut (UConn) found people, particularly minorities, got tripped up on the word “premium,” while others couldn’t calculate their out-of-pockets costs.

“Having health insurance is an invaluable asset, but what good is it if people can’t understand how to use it?” asked Victor Villagra, MD, FACP, associate director of the Health Disparities Institute at UConn Health, in a UConn Today story on the data.

Many people have employer-offered health packages, which can be less overwhelming because the employer does most of the heavy lifting, offering up several options tailored by the organization.

Buying individual health insurance through the ACA can be more involved, so the probability that someone needs help through the process is higher. Also, many enrollees are new to insurance, like millennials no longer on their parent’s coverage, or from lower socioeconomic groups, which have historically higher rates of low health literacy.

The architects of the ACA knew all of this, so resources were funneled toward web content development and navigators to help guide people through such complex waters. Nonprofit health centers and organizations throughout the country took it on, as well, building outreach programs to educate and enroll people.

It has been no easy task.

People need information in an understandable language, said Karen Pollitz, of the Kaiser Family Foundation, last year at a roundtable on health literacy at the National Academies of Sciences, Engineering in Washington, D.C., a brief from the National Academies reported. But they also “need to sit down with an expert who can hold their hand and walk [them] through this process.” Even after three years, she said, it takes “an experienced navigator an average of 90 minutes to guide a person through the process of determining eligibility and enrollment.”

These efforts helped get more people insured, but resources have dried up, and attention has shifted with the change in administrations. And there are still millions without insurance.

At that same roundtable, Elisabeth Benjamin, of the Community Service Society of New York, pointed to another barrier, this one beyond the consumer. “I feel like a lot of education needs to happen on the [health care] provider side about insurance,” she said. “I think a lot of providers do not really understand insurance.”

A trend that has taken off are the pop-up boxes defining words and out-of-pocket cost calculators on governmental and state health care websites, two features that millennials also asked for in the 2015 Penn study.

“Health insurance literacy is step one – and part of that is being able to apply those terms,” said Charlene A. Wong, MD, a former Robert Wood Johnson Foundation Clinical Scholar and LDI fellow at Penn who is now at Duke University, and first author of that Penn study. “Step two is numeracy. These cost estimators, which more and more sites are providing, do the math for you.”

The tool helps people take a step back to get a better picture of their totals costs, including premiums and out-of-pocket costs, rather than just homing in on their premiums (monthly costs), and sort plans accordingly.

“They are trying to be smart with this by creating a choice architecture for the consumer to more easily understand the choices that may be best for them,” Polsky said. “That’s where the advances come in.”

Polsky and Wong have been studying the frequency and impact of these features, with new data expected to be released this year.

Efforts to inform people – and enroll them – continue, but with the fate of the ACA hanging in the balance, it remains to be seen how the knowledge gap will be addressed.

“This is a tough problem to solve on a societal basis. We really have to put in the resources to fill this gap, and it’s something that has to be there in the future,” Polsky said. “A nonstop door-to-door campaign that is constant – and always.”